Four steps to calculate the manufacturing cost of sheet metal products

In today’s competitive markets, understanding the structure of the costs of a product is essential to the improvement of the process as well as to a correct pricing strategy.

The production cycle of a sheet metal product involves several phases from the raw material to the product ready for delivery which include: cutting, roll forming, bending, welding, punching, laser cutting, assembly of possible accessories, painting and packaging.

My previous articles are focused on:

- Understanding the scrap rate generated by different cutting processes

- How to calculate the hourly cost and rate of a sheet metal production system

- How to calculate the productivity and efficiency of a sheet metal production system

We have seen how some of these parameters, for example the Efficiency of a machine or its Hourly Cost, depend from a number of estimations and strategic decisions the entrepreneur has to take. We have always to bear in mind, that the result of the calculation will be affected by all these decisions.

Here, I will use some of the concepts and ideas of these articles and propose a method to estimate the production cost of a single sheet metal product, and of a full batch.

You can find more details related to these concepts into the book “The Revolution of Efficiency” that you can request here:

REQUEST THE BOOK FOR FREE

Dallan develops efficient technologies and machines in order to improve the production cycle and to break down production costs. This is possible thanks to the optimization of raw material utilization (up to 100%), and making maintenance cost even more cost-effective.

Discover all the Dallan technologies and the production systems:

| Roll forming machines | Punching machines | Laser cutting machines |

Step one: breaking down the production cycle

The formulas described in the previous article are meant to calculate the hourly cost and efficiency of a single machine or system.

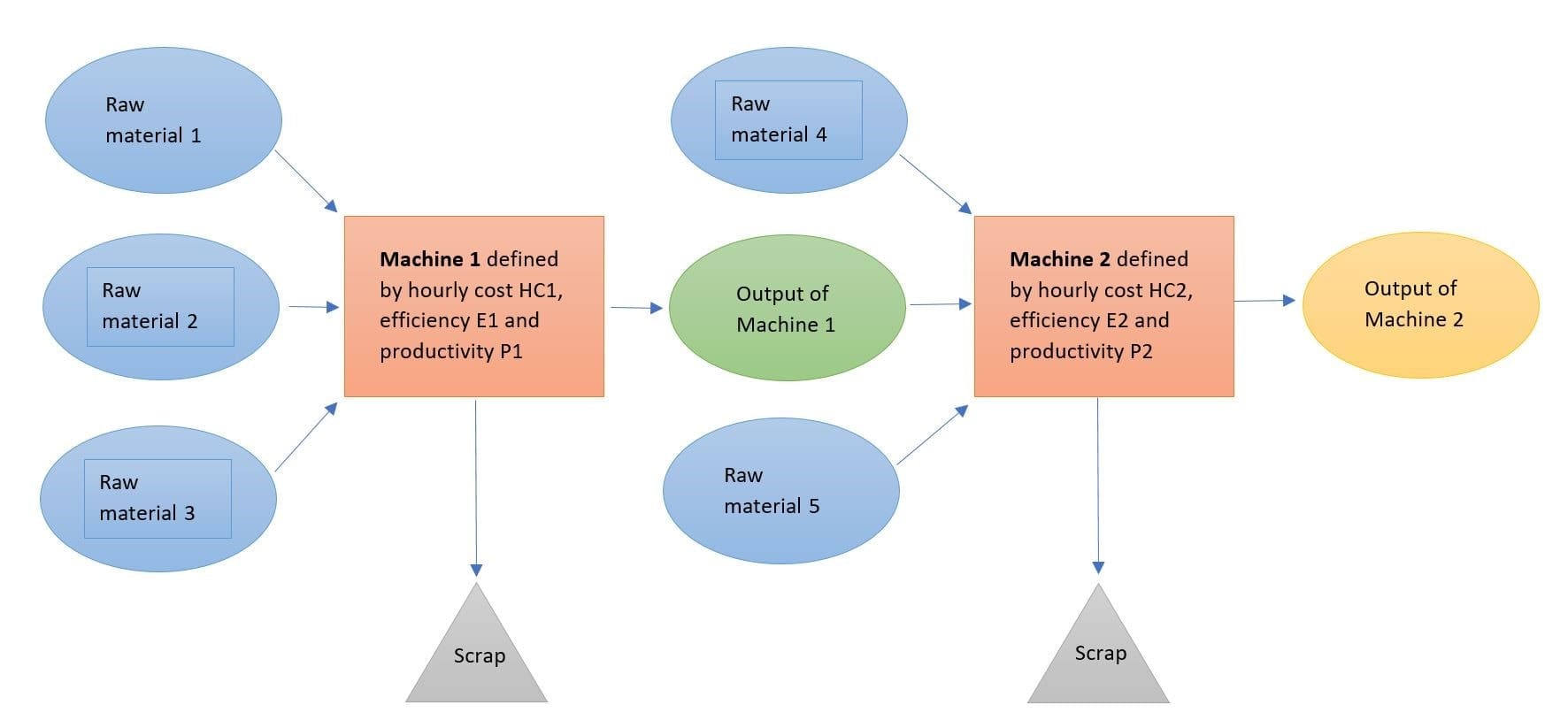

Since production cycles can be so different from one another, and may include different phases, we need to brake the production cycle down to simpler processes, as shown in the picture below.

In this way the output of Machine 1 becomes the input of Machine 2, carrying on its production cost as if it were a new raw material.

Now, it is possible to focus on one of these production cycles at a time. Let’s start from Machine 1.

Step two: calculate the cost of the raw materials

The manufacturing of one product requires one or more types of raw materials.

For example, a standalone roll former for drywall studs requires coils of galvanized steel. In the case it is a complete system with roll forming and packaging, the raw materials will be: metal coils, straps and timber tiles.

At this point, we need to calculate or estimate the amount of raw material that will be required to manufacture one single product, including the scrap generated in the process. In the first article, I showed how Elleci could generate an average gain of 15,9% on the raw material costs, by moving a set of articles to more efficient technologies.

Let’s take as an example the product F of the a.m. article. The product has dimensions 415x685mm, thickness 1mm and is obtained from a sheet metal plate with dimension 1000×2100. We can fit 6 parts in this sheet, with a scrap of 19%. In this case, we need to consider that the amount of raw material per one piece is a plate with dimensions 700x500mm, thickness 1mm.

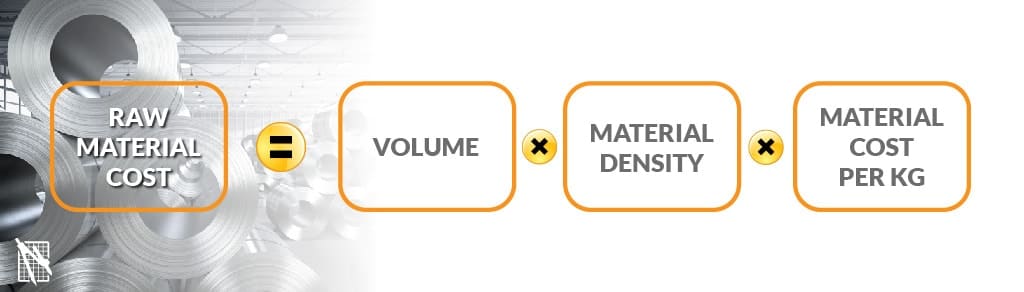

The cost of the raw material per one piece is given by this formula:

In the previous example, assuming 0,7 Euro per kg as the Material cost per kg, and density of steel 7,8 kg/dm3 we obtain:

RAW MATERIAL COST = 7 * 5 * 0,01 * 7,8 * 0,7 = 1,91 Euro

This procedure has to be repeated with each of the raw materials entering the process.

Step three: adding the cost of the machining

At this point, we need to have the following data:

- Hourly cost of the machine or system, as calculated with the method illustrated in the second article. In this phase, we will not take into account the overhead costs.

- Productivity (cycle time) and Efficiency of the system, as calculated in my third article.

The formula to calculate the cost of the machining is the following:

For example, with a cycle time of 12 seconds, efficiency 80,5% and a Machine hourly cost of 77,3 Euro we obtain:

MACHINING COST = 77,3 * 12 / 0,805 / 3600 = 0,32 Euro

So the total direct cost of the production for one piece is:

And in our example:

TOTAL PRODUCT COST IN MACHINE 1 = 1,91 + 0,32 = 2,23 Euro

In this case, the cost of the machining represents just the 14% of the total cost of the product, where the raw material represent the remaining 86%. These percentages may vary, but it is clear that any saving in the raw material (with the optimization or elimination of the scrap) can be highly beneficial to the overall production cost.

In some productions, we may need to produce a specific tooling that cannot always be calculated as a part of the machine.

In this case I prefer to see it as a part of the investment to complete the production of N parts, and use this formula:

(Total production cost) = N*(Raw material cost) + N*(Hourly Cost)*(Cycle time per one piece) /(Efficiency) + Tooling costs

Note that this formula is slightly different from the one I suggested in the article about the hourly cost, since the setup time is already taken care of by the Efficiency.

Dallan develops lean production systems and highly efficient machines. The latest innovation regards the sheet metal laser cutting applied to in-line coil fed production. Pluriannual Dallan experience in in-line production systems allowed us to develop a revolutionary laser cutting machine that joins the flexibility and cost-effectiveness of fiber laser cutting with the efficiency and productivity of coil-fed production.

Step four: repeating the calculation for the different phases of the production cycle

Now that we have calculated the production cost from raw material to the output of machine 1, we can repeat the procedure for the other machines or phases that complete the production cycle.

The output of each machine carries on the costs attached to it by the previous processes, until the end of the line is reached and the product is ready for the delivery.

The 80/20 rule applied to the structure of the product cost

The simple methodology illustrated in this article can lead to significant insights about the structure of the product cost, as well as helping to identify where to act to improve the profitability of a product or product line.

In the above example, with the cost of the raw material being 86% of the total cost, it is clear that any % in saving in the raw material (for example by reducing the scrap rate) will lead to a proportional reduction of the total product cost.

In a production cycle that includes several phases, it will be possible to understand how each phase contributes to the total industrial cost making it possible, for the production manager, to prioritize the interventions for the improvement of the process.

As deep connoisseur in sheet metal working processes, Dallan focused its development in highly efficient production systems and technologies. In-line, coil-fed philosophy ensures the highest optimization in raw material utilization, meaning less scraps and more revenue than traditional systems. Moreover innovative and sustainable technologies guarantee a reduction of operating and maintenance costs.

REQUEST THE BOOK FOR FREE

Important note

In the introduction of the article I pointed out that the output of this methodology is an estimation of the total product cost, since several of the parameters we use are the result of a decision or estimation of the production manager.

In addition to that, note that this method does not take into account the logistic costs due to storing and moving the products from one machine or process, to the next. If this process is manual, these costs can be an important part of the total cost and they should be estimated by the production manager. For this reason the production in line is always preferable.

Anyway if the logistic of the products between two machines is automatic and carried on, for example, by a machine or automatic storage, this phase could be considered as another phase of the process, where the automatic storage is another machine characterized by its Hourly Cost and by a Cycle time that is the highest of the cycle times of the machines that come upstream and downstream.

Conclusions

This article completes the series of articles dedicated to the calculation of the machine hourly cost, efficiency and scrap rate.

In the previous articles, I highlighted the factors that the entrepreneur and the production manager have to consider when deciding the machines hourly cost and rate, and the importance of the organization of the production in order to guarantee the high efficiency of machines and systems.

Modern production systems allow for fast, automatic and highly efficient production, where setup times for tool change are constantly reduced or – as in the case of laser cutting machines – eliminated.

Even with highly automated system, often the cost of the machining represents a smaller percentage of the raw material cost. For this reason, any saving in the raw material cost in terms of scrap reduction becomes highly beneficial in terms of reduction of the overall industrial cost.

Contact our engineers HERE